Watching your parents age brings a shift in responsibility that many of us aren’t prepared for. The roles reverse slowly, then all at once. One day you notice unpaid bills on the kitchen table. Or your mum mentions she’s not sure how much CPF she has left. These small moments signal it’s time to have conversations that feel uncomfortable but matter deeply.

As your parents enter their later years, understanding their financial situation becomes essential for their wellbeing and your peace of mind. This guide covers the critical financial questions to ask aging parents, from CPF balances and retirement income to healthcare coverage and estate planning. Having these conversations early helps prevent future complications and ensures your parents receive the support they deserve during their retirement years.

Why talking about money with your parents feels so hard

Money conversations carry emotional weight in Asian families. Many seniors view discussing finances as a loss of independence or dignity. They may feel embarrassed about their savings, protective of their privacy, or worried about burdening their children.

Your parents likely spent decades supporting you. Accepting that they now need your help represents a fundamental shift in family dynamics. This discomfort is normal on both sides.

But avoiding these conversations creates bigger problems down the line. Without knowing their financial situation, you can’t help them access benefits they’re entitled to or prevent costly mistakes. You might miss critical deadlines for government healthcare subsidies or discover financial issues only when they’ve become emergencies.

The key is approaching these discussions with respect and patience. Frame questions as wanting to help them maximise what they’ve worked for, not as checking up on them.

Setting up the conversation properly

Choose the right moment. Don’t ambush your parents during a family gathering or when they’re stressed. Instead, suggest a dedicated time to discuss their plans and how you can support them.

Start by sharing your own financial plans if appropriate. This creates reciprocity and shows you’re not just prying. You might mention your own CPF planning or insurance reviews to normalise the conversation.

Bring your siblings into the discussion if possible. Having everyone on the same page prevents misunderstandings and distributes caregiving responsibilities more fairly. It also shows your parents that the whole family is invested in their wellbeing.

Be prepared for resistance. Your first attempt might not go smoothly. That’s fine. Plant the seed and return to it later. Sometimes parents need time to process that this conversation is necessary.

The essential financial questions every caregiver must ask

1. What are your monthly expenses and income sources?

Understanding the basics comes first. Ask your parents to walk you through a typical month. What bills do they pay? What income do they receive?

Many Merdeka Generation seniors have multiple income streams. CPF LIFE payouts form the foundation for most. Some receive pension income from previous employment. Others have rental income, part-time work, or support from children.

On the expense side, look for patterns. Are they spending more on healthcare than expected? Do they have subscription services they’ve forgotten about? Are utility bills reasonable for their flat size?

This baseline picture helps you spot problems early. If expenses consistently exceed income, you’ll need to address it before savings run dry.

2. How much do they have in their CPF accounts?

CPF balances determine retirement security for most Singaporeans. Your parents should know their balances across all three accounts and their monthly CPF LIFE payout amount.

If they’re unsure, help them check via the CPF website or mobile app. Understanding whether they can withdraw their CPF savings at 65 depends on their specific situation and account balances.

Pay attention to their Medisave balance. This account covers medical expenses and insurance premiums. If it’s running low, you might need to consider topping up their MediSave to ensure adequate healthcare coverage.

Also check if they’ve maximised their CPF LIFE payouts. Some seniors don’t realise they can stretch their CPF LIFE payouts further through various strategies.

3. What healthcare coverage do they have?

Healthcare costs rise dramatically with age. Knowing your parents’ coverage prevents nasty surprises when medical needs arise.

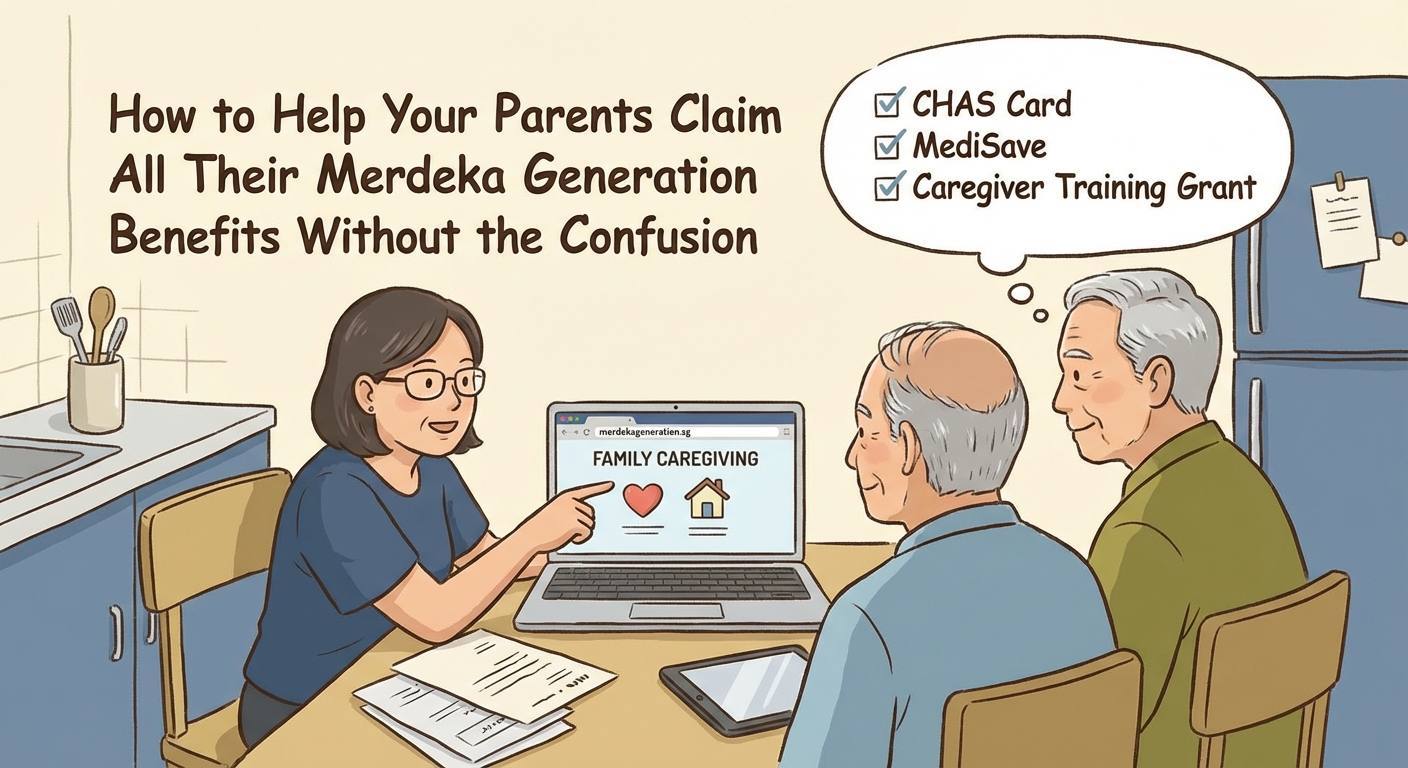

Start with government schemes. If your parents were born between 1950 and 1959, they likely qualify for Merdeka Generation benefits. Check if they’ve registered and understand how to claim all their benefits properly.

Ask about their MediShield Life coverage. All Singapore citizens have this basic health insurance, but maximising MediShield Life coverage requires understanding the details.

Check if they have Integrated Shield Plans for additional private coverage. Review their CHAS card status for subsidised outpatient care. Understanding CHAS card benefits helps them access affordable healthcare.

Don’t forget dental coverage. Many seniors neglect oral health due to cost, but subsidies exist for those who qualify.

4. Do they have proper estate planning documents?

Estate planning sounds morbid but protects everyone. Ask if your parents have made a will, appointed someone with Lasting Power of Attorney, and documented their end-of-life wishes.

A will ensures their assets go where they want them. Without one, intestacy laws decide, which may not match their intentions. This matters especially if they have property, savings, or specific wishes about distributing their estate.

Lasting Power of Attorney lets trusted individuals make decisions if your parents lose mental capacity. This covers both property and personal welfare decisions. Setting this up while they’re still mentally sharp prevents complications later.

CPF nominations deserve special attention. What happens to CPF savings when they pass away depends on whether they’ve made proper nominations. Without nominations, CPF savings may be tied up in lengthy estate proceedings.

5. Where do they keep important documents?

In an emergency, you need to access critical information fast. Ask your parents where they store important documents and how you can access them if needed.

Create a list together of document locations. This includes identity cards, property deeds, insurance policies, bank statements, CPF statements, and medical records. Note where physical documents are kept and login details for online accounts.

If they’ve lost important documents like their Merdeka Generation card, help them get replacements now rather than during a crisis.

Consider setting up a shared secure folder or safe deposit box. Make sure at least one trusted family member knows how to access everything.

6. What are their housing plans?

Housing represents most Singaporeans’ largest asset. Understanding your parents’ housing situation and plans helps with long-term financial planning.

Do they own their flat outright or still have mortgage payments? If they’re considering downsizing their HDB flat for extra retirement cash, discuss the pros and cons together.

Some seniors explore the Lease Buyback Scheme. Understanding whether they should lease back their flat requires careful consideration of their financial needs and housing preferences.

Also discuss their preferences for aging in place versus moving to senior housing. Choosing between ageing-in-place and sheltered housing involves both financial and lifestyle considerations.

7. Are they managing their bills and avoiding scams?

Cognitive decline can happen gradually. Watch for signs your parents are struggling with financial management.

Ask to review their bank statements together. Look for unusual transactions, duplicate payments, or unfamiliar charges. Seniors are prime targets for scams, from fake government officials to investment frauds.

Check if bills are being paid on time. Late payments might indicate confusion, forgetfulness, or financial strain. Consider setting up GIRO for regular bills if they’re struggling to keep track.

If they’re receiving calls about investments or prizes, discuss common scam tactics. Many seniors feel embarrassed admitting they’ve been targeted, so approach this with sensitivity.

8. How much do they really need for retirement?

Many seniors worry about outliving their savings. Help your parents calculate how much money they really need for retirement based on their actual lifestyle and expenses.

Work through their budget together. Factor in regular expenses, healthcare costs, occasional treats, and emergency buffers. This exercise often reveals they’re more secure than they thought, or highlights gaps that need addressing.

If there’s a shortfall, explore options. Can they reduce expenses? Are there benefits they’re not claiming? Would part-time work or safe side hustles supplement their income comfortably?

Help them create a monthly budget that works with their fixed income sources. This provides clarity and reduces financial anxiety.

Common mistakes to avoid during these conversations

| Mistake | Why It’s Harmful | Better Approach |

|---|---|---|

| Being judgmental about past decisions | Damages trust and makes parents defensive | Focus on solutions for the future |

| Taking over completely | Removes their autonomy and dignity | Support their decision-making rather than replacing it |

| Having the conversation in one sitting | Overwhelms everyone involved | Break into multiple shorter discussions |

| Excluding siblings | Creates family conflict later | Keep everyone informed and involved |

| Waiting for a crisis | Limits options and increases stress | Start conversations while everyone is healthy |

| Forgetting to listen | Misses important context and preferences | Ask open-ended questions and truly hear responses |

Making the most of available benefits and support

Singapore offers substantial support for seniors, but many don’t claim everything they’re entitled to. Your role includes helping your parents navigate these systems.

The Merdeka Generation Package provides significant healthcare subsidies and support. If you’re unsure about eligibility, learn how to check if they qualify and help them avoid common mistakes when claiming benefits.

Look beyond healthcare subsidies. Managing healthcare costs in retirement involves multiple strategies, from preventive care to smart use of subsidies.

Don’t overlook everyday savings. Help them maximise grocery shopping with senior discount days and access public transport concessions.

“The biggest gift you can give aging parents is helping them maintain dignity while ensuring they’re financially secure. It’s not about taking control but about providing support so they can continue making informed decisions about their own lives.” – Financial counsellor specialising in elder care

When professional help makes sense

Some situations require expertise beyond family knowledge. Don’t hesitate to bring in professionals when needed.

Financial advisers who specialise in retirement planning can review your parents’ situation objectively. They might spot opportunities or risks you’ve missed.

Elder law attorneys help with complex estate planning, especially if there are disputes, overseas assets, or complicated family situations.

Social workers at Family Service Centres provide practical support and can connect you with community resources. They’re especially helpful if financial stress is affecting family relationships.

Accountants can help with tax planning, especially if your parents have rental income or are considering whether to top up CPF LIFE after 65.

Ongoing financial check-ins

One conversation isn’t enough. Financial situations change, as do needs and capabilities.

Schedule regular check-ins. Quarterly reviews work well for most families. Use these sessions to review spending, discuss any concerns, and adjust plans as needed.

Watch for changes in behaviour. Is your mum suddenly anxious about money despite having adequate savings? Is your dad making impulsive purchases? These might signal cognitive changes requiring additional support.

Keep siblings updated. Regular family meetings, even brief ones, prevent misunderstandings and ensure everyone shares caregiving responsibilities fairly.

Document important information. Keep a shared file with account numbers, contact information for advisers, and notes from your conversations. This becomes invaluable during emergencies.

Practical tips for different family situations

If your parents are still working: Focus on maximising CPF contributions and understanding their retirement timeline. Discuss when they plan to stop working and how that will affect their income.

If they’re newly retired: Help them adjust to fixed income living. The transition from earning to drawing down savings feels uncomfortable for many. Build confidence in their retirement plan.

If one parent has passed away: Review everything. Survivor benefits, CPF payouts, housing arrangements, and healthcare coverage all need reassessing. The surviving parent’s financial situation has changed significantly.

If parents are divorced or separated: Navigate carefully. Each parent’s situation is unique. Don’t assume their financial arrangements mirror typical patterns.

If they’re planning to move overseas: Understand how this affects their benefits. Moving overseas after retirement has implications for government support and healthcare coverage.

Building a support network

You don’t have to manage everything alone. Build a network of support for both your parents and yourself.

Connect with other caregivers. Many community centres run caregiver support groups. Sharing experiences with others in similar situations provides practical advice and emotional support.

Explore community resources. Senior activity centres, day rehabilitation programmes, and befriending services provide social engagement and support. Understanding whether senior activity centres or day rehabilitation better suits their needs depends on their health and preferences.

Look into affordable active ageing programmes that keep your parents engaged and healthy. Social connection matters as much as financial security for quality of life.

Consider respite care options. Caregiving is demanding. Having backup support prevents burnout and ensures you can provide sustainable help over the long term.

Planning for long-term care needs

Healthcare needs typically increase with age. Planning ahead reduces stress when issues arise.

Discuss preferences for care. Would your parents prefer home care or residential care if they need daily assistance? What level of medical intervention do they want? These conversations are difficult but essential.

Research care options and costs now. Nursing homes, home care services, and day care centres all have different costs and benefits. Knowing what’s available helps you make informed decisions later.

Review insurance coverage for long-term care. Some policies include riders for nursing home care or home care. Understand what’s covered and what isn’t.

Consider the financial impact of different care scenarios. How long could their savings last if they need full-time care? Would you need to supplement their finances? Planning for these possibilities prevents panic later.

Teaching your parents about digital financial tools

Many seniors feel intimidated by online banking and digital government services. Patient teaching helps them maintain independence longer.

Start with basic online account access. Help them set up and practise using internet banking in a safe environment. Write down login steps clearly.

Show them how to check CPF balances online. The CPF website and mobile app provide real-time information. Being able to check independently reduces anxiety.

Introduce them to useful apps gradually. PayNow for transfers, government apps for claiming subsidies, and health apps for tracking medical information all improve convenience once they’re comfortable.

Always prioritise security. Teach them to recognise phishing attempts, never share passwords, and verify requests before making transfers.

Respecting their autonomy while providing support

The balance between helping and controlling is delicate. Your goal is supporting your parents’ independence, not replacing it.

Let them make decisions whenever possible. Offer information and advice, but respect their choices even if you’d decide differently. Their money and their life remain theirs.

Recognise that their priorities might differ from yours. They might value experiences over savings, or prefer staying in their current home despite financial benefits of moving. That’s their right.

Watch for signs they truly can’t manage anymore. Unpaid bills, falling for scams repeatedly, or confusion about basic finances signal it’s time for more direct intervention. But reach this conclusion based on evidence, not assumptions.

Involve them in all decisions that affect them. Don’t make arrangements without their input. Even if their capacity is declining, include them in discussions and honour their preferences wherever possible.

Supporting your parents without sacrificing your own financial security

Helping your parents financially can strain your own resources. Set boundaries that protect your future while supporting theirs.

Don’t sacrifice your retirement for theirs. You can’t turn back time on CPF contributions or lost investment years. Find sustainable ways to help that don’t jeopardise your own security.

Be clear about what you can and can’t provide. If you’re contributing financially, decide on an amount you can sustain long-term. Don’t overcommit and then have to pull back.

Explore all available support before using your own money. Government subsidies, community programmes, and their own resources should be maximised first.

Consider tax implications of financial support. Some contributions to parents’ accounts offer tax relief. Understand these benefits before making decisions.

Moving forward with confidence and care

These conversations about financial questions to ask aging parents mark a significant transition in your family relationships. They’re rarely easy, but they’re always worthwhile.

Start small if the topic feels overwhelming. Pick one question from this guide and begin there. Build trust and comfort gradually. Each conversation makes the next one easier.

Remember that you’re not alone in this journey. Thousands of families across Singapore are having similar conversations. Resources exist to help you. Community support is available. Professional guidance is accessible.

Your parents worked hard to build their retirement security. Your role is helping them maximise what they’ve created, access benefits they’ve earned, and maintain dignity throughout their later years. Approach these conversations with love, patience, and respect. The temporary discomfort of discussing money matters far less than the lasting peace of mind you’ll all gain from proper planning and open communication.