Thinking about downsizing your HDB flat to boost your retirement funds? The Silver Housing Bonus (SHB) scheme can put up to $30,000 into your CPF Retirement Account when you move to a smaller home. But many seniors miss out simply because they don’t know the application steps or assume the process is too complicated.

The Silver Housing Bonus gives eligible seniors aged 65 and above up to $30,000 when they downsize to a smaller HDB flat. You apply through HDB when purchasing your replacement flat, and the bonus goes directly into your CPF Retirement Account. Your household income and property ownership affect your eligibility, and you must meet specific conditions including maintaining a minimum CPF balance after the move.

Who can receive the Silver Housing Bonus

Before you start the application, make sure you meet the basic requirements.

You must be at least 65 years old when you apply. Your spouse, if you’re applying as a couple, must also be 65 or above.

Your current flat must be a 3-room or larger HDB unit. You’ll be moving to a smaller flat, either a 2-room Flexi or 3-room flat.

Average gross household income matters. If you’re single, your monthly income must not exceed $6,000. For couples or families, the combined household income cap is $12,000 per month.

Property ownership affects your eligibility too. You can own only one property at the time of application, which is the flat you’re selling. If you or anyone in your household owns other properties, including private property, you won’t qualify unless the total annual value of all properties stays below $21,000.

You must not have received the Silver Housing Bonus before. This is a one-time benefit.

“Many seniors think they don’t qualify because they have some savings or own their flat outright. The scheme actually looks at your monthly income and property ownership, not your total wealth. Don’t rule yourself out before checking the full criteria.” (HDB eligibility guidelines)

Understanding your bonus amount

The Silver Housing Bonus isn’t a fixed sum. Your bonus amount depends on your replacement flat type and your property ownership situation.

If you’re moving to a 2-room Flexi flat, you can receive up to $30,000. Moving to a 3-room flat gets you up to $15,000.

But there’s a catch. If you or anyone in your household owns any other property, including private property with annual value, your bonus gets reduced by $1 for every $1 of annual value above $0, up to $21,000.

Here’s how it works in practice:

| Your situation | Replacement flat | Maximum bonus |

|---|---|---|

| No other property | 2-room Flexi | $30,000 |

| No other property | 3-room flat | $15,000 |

| Own property with $10,000 annual value | 2-room Flexi | $20,000 |

| Own property with $15,000 annual value | 3-room flat | $0 |

The bonus goes straight into your CPF Retirement Account. You cannot receive it as cash. This ensures the money supports your retirement income through CPF LIFE payouts.

Checking your CPF balance requirements

The Silver Housing Bonus comes with a mandatory CPF top-up requirement. This ensures you maintain adequate retirement savings after downsizing.

After you sell your current flat and buy the smaller one, you must have at least $60,000 in your CPF Retirement Account. This includes the Silver Housing Bonus amount.

If you’re applying as a couple, each person must meet this $60,000 threshold individually. Your spouse’s CPF balance doesn’t count towards your requirement.

Let’s say you currently have $40,000 in your CPF Retirement Account. You’re moving to a 2-room Flexi flat and qualify for the full $30,000 bonus. After the sale proceeds are used for the new flat purchase and the bonus is credited, you’d have $70,000. That meets the requirement.

But if you only have $20,000 in your CPF Retirement Account, even with the $30,000 bonus you’d only reach $50,000. You’d need to top up an additional $10,000 from your sale proceeds to meet the $60,000 minimum.

Planning ahead helps. Before you commit to selling, calculate your expected CPF balance after the transaction. Factor in your current balance, the bonus amount, and how much of your sale proceeds you’ll need for the new flat purchase.

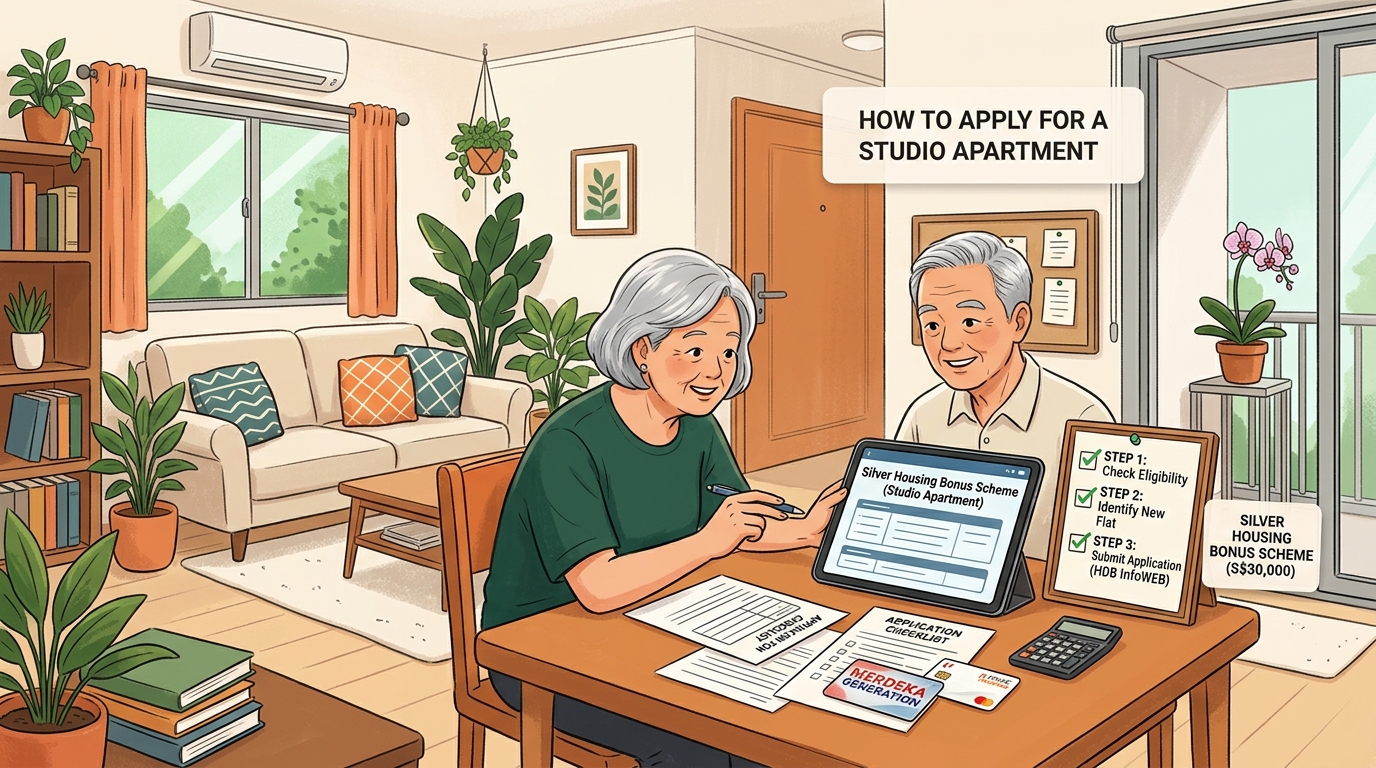

Step by step application process

The application happens during your flat purchase, not as a separate process. Here’s exactly what to do.

1. Get your HDB Flat Eligibility letter

Start by applying for an HDB Flat Eligibility (HFE) letter. You can do this online through the HDB website or at any HDB branch.

You’ll need your Singpass to log in. The system will ask about your household members, income, and current property ownership.

Indicate that you want to apply for the Silver Housing Bonus during this HFE application. The system will check your eligibility automatically.

Processing takes about 3 weeks. You’ll receive a letter stating whether you’re eligible for the scheme and your estimated bonus amount.

2. Book your replacement flat

Once you have your HFE letter, you can book a flat. This applies whether you’re buying from HDB directly or from the resale market.

For new flats, participate in the HDB sales exercise. Your HFE letter confirms your eligibility for priority schemes if applicable.

For resale flats, find a suitable unit and negotiate with the seller. Your HFE letter remains valid for 6 months, giving you time to search.

Make sure the flat you’re buying is smaller than your current one. A 2-room Flexi or 3-room flat qualifies.

3. Submit your resale application

If you’re buying a resale flat, both buyer and seller submit the resale application through the HDB resale portal.

During this application, you’ll confirm that you’re applying for the Silver Housing Bonus. The system will calculate your exact bonus amount based on your circumstances.

You’ll also see the CPF balance requirement clearly stated. The system shows how much you need to set aside in your CPF Retirement Account.

4. Complete the flat purchase

Attend the HDB appointment to complete the purchase. Bring all required documents including identification, income proof, and your HFE letter.

HDB will verify your eligibility again at this stage. They’ll check that your circumstances haven’t changed since your HFE approval.

Sign all necessary documents. The flat purchase completes, and ownership transfers to you.

5. Receive your bonus

After completion, HDB credits the Silver Housing Bonus directly to your CPF Retirement Account. This happens automatically within a few weeks.

You’ll receive a notification from CPF showing the credit. Check your CPF statement online to confirm the amount.

The bonus becomes part of your CPF LIFE plan, generating monthly payouts during retirement. You cannot withdraw it as a lump sum.

Common mistakes that delay applications

Many seniors run into problems that could have been avoided with better preparation.

Not checking income limits carefully

Some applicants forget to include all household income sources. Rental income, part-time work, and regular financial support from children all count. If your total exceeds the cap, you won’t qualify. Calculate accurately before applying.

Overlooking property ownership rules

Owning a small investment property or having your name on a family member’s property title can disqualify you. Even if you don’t live there or don’t benefit financially, HDB considers it property ownership. Check all property records before starting your application.

Selling current flat before securing replacement

You need to own your current flat when you apply. Some seniors sell first, thinking they can apply later. That doesn’t work. Apply while you still own the flat you’re downsizing from.

Insufficient CPF balance planning

Not having enough in your CPF Retirement Account to meet the $60,000 requirement stops many applications. Calculate this before you commit to selling. You might need to set aside more sale proceeds than expected.

Missing the HFE validity period

Your HFE letter expires after 6 months. If you don’t find a replacement flat within that time, you need to reapply. Start your flat search early to avoid rushing or missing the deadline.

Assuming automatic approval

Meeting the basic criteria doesn’t guarantee approval. HDB reviews each application individually. Provide complete, accurate information and respond to any queries promptly.

What happens after you receive the bonus

Getting the Silver Housing Bonus is just the beginning. Understanding how it affects your retirement planning matters.

The bonus sits in your CPF Retirement Account and becomes part of your CPF LIFE plan. This means it generates monthly payouts from age 65 onwards.

For example, if you receive the full $30,000 bonus, this increases your monthly CPF LIFE payout. The exact increase depends on your CPF LIFE plan type and your age when the bonus is credited.

You cannot withdraw the bonus as cash, even after age 65. It stays locked in CPF LIFE to provide retirement income. This protects you from spending the money too fast.

If you’re thinking about how this fits with other retirement planning strategies, should you downsize your HDB flat for extra retirement cash covers the broader financial considerations.

The bonus also counts when calculating your CPF balances for other purposes. If you’re planning to top up your CPF further, should you top up your CPF LIFE after 65 explains how additional contributions work with existing balances.

Coordinating with other retirement benefits

The Silver Housing Bonus works alongside other government schemes available to seniors.

If you’re part of the Merdeka Generation, you already receive healthcare subsidies and other benefits. The Silver Housing Bonus doesn’t affect these. You keep all your existing benefits.

However, if you’re unsure about your Merdeka Generation eligibility status, how to check if you qualify for the Merdeka Generation Package in 2024 walks through the verification process.

Some seniors worry about losing benefits when they move. Your CHAS card benefits continue at your new address. The healthcare subsidies don’t change based on your flat size. Learn more about CHAS card benefits explained to understand what remains available.

Your MediShield Life coverage also stays active. Moving to a smaller flat doesn’t affect your healthcare protection. For details on maximizing this coverage, how to maximise your MediShield Life coverage as a Merdeka Generation senior provides practical strategies.

Planning your finances after downsizing

Downsizing creates a significant financial shift. The Silver Housing Bonus is one part, but you’ll also have cash proceeds from selling your larger flat.

Most seniors use sale proceeds to pay for the smaller replacement flat. The leftover amount can supplement retirement income or serve as emergency savings.

Consider how much you need for monthly expenses. Your CPF LIFE payouts, including the boost from the Silver Housing Bonus, provide baseline income. Cash savings cover unexpected costs.

Healthcare expenses often increase with age. While MediShield Life and CHAS subsidies help, some costs still come out of pocket. Managing healthcare costs in retirement offers strategies for handling medical expenses beyond subsidies.

Creating a realistic budget helps you live comfortably on fixed income. Creating a monthly budget that works on fixed CPF LIFE and pension income shows how to structure spending when your income doesn’t fluctuate.

Documents you’ll need throughout the process

Gather these documents before starting your application to avoid delays.

- NRIC for all household members applying

- Recent payslips or income statements covering the last 12 months

- CPF contribution history printout from the CPF website

- Current flat ownership documents showing you as the registered owner

- Property tax statements if you own any other property

- HDB Flat Eligibility letter once approved

- Resale flat listing or booking documents for your replacement flat

Keep both physical and digital copies. Some appointments require original documents, while online applications need scanned versions.

If you’re missing any documents, request them early. CPF statements take a few days to generate. Property ownership searches through IRAS can take up to a week.

Getting help with your application

You don’t have to figure this out alone. Several resources can guide you through the process.

HDB branches offer face-to-face assistance. Staff can review your eligibility, explain requirements, and help with online submissions. Book an appointment to avoid long waits.

The HDB hotline answers questions about the scheme. Call 1800-225-5432 during office hours. Have your NRIC ready for identity verification.

Community centres and senior activity centres sometimes run workshops on housing schemes for elderly residents. These sessions explain the process in simple terms and answer common questions.

If you prefer written guidance, the HDB website has detailed information pages. Search for “Silver Housing Bonus” to find official guidelines, eligibility criteria, and application instructions.

For seniors who need help avoiding common pitfalls with government benefits, 5 common mistakes Merdeka Generation seniors make when claiming benefits highlights issues to watch for.

Making the most of your downsizing decision

Applying for the Silver Housing Bonus is straightforward when you know the steps. Start by checking your eligibility carefully, especially income limits and property ownership. Get your HFE letter early to allow time for flat hunting. Calculate your CPF balance requirements before committing to sell. Follow the application process during your flat purchase, not as a separate task.

The bonus boosts your retirement income through higher CPF LIFE payouts. Combined with proceeds from selling your larger flat, downsizing can significantly improve your financial security in retirement. Take time to plan how you’ll use both the bonus and any cash proceeds wisely.

Don’t let uncertainty stop you from exploring this option. Thousands of seniors have successfully applied for the Silver Housing Bonus and moved to comfortable, more manageable homes. With proper preparation and understanding of the process, you can too.

Leave a Reply